DeFi Pulse Index Monthly Update - April 2021

DeFi Pulse Index Monthly Update - April 2021

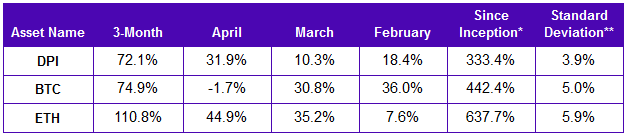

DPI outperforms BTC while ETH breaks out in April.

April saw a considerable decoupling of correlation and returns between BTC and ETH. Bitcoin traded lower to end the month down -1.7% versus ETH’s return of +44.9%. Meanwhile, DPI returned +31.9% over the same period.

In the last 3 months, DPI has performed in line with BTC but has lagged ETH by -38.7%. However, DPI is still the leader year-to-date (+369.3%) compared to BTC (+99.3%) and ETH (+275.9%).

Product Growth

The DPI product continues to see widespread adoption, especially among smaller holders as evidenced by the following Dune Analytics graph courtesy of JD Cook. During the month of April, addresses holding less than 10 units of DPI grew by +6.4% and are up +234% since the start of the year. The total number of addresses holding DPI stood just shy of 13,000 on April 30th. This threshold was subsequently broken on May 3rd.

Strong growth in the total number of holders makes sense given DPI is a low-cost way of getting exposure to the DeFi sector within a single token.

Portfolio Analytics

Digging in a bit, an analysis of upside and downside capture ratios reveals a strong positive net capture rate for DPI relative to BTC. DPI had briefly managed to capture a net positive rate relative to ETH toward the beginning of the year but has been unable to continue the trend since. As a reminder, a positive net capture ratio means an asset is capturing more upside performance than downside performance relative to another asset.

When looking at correlation and beta metrics, DPI remains additive to portfolio diversification. The current correlation to BTC stands at 0.45 while the correlation to ETH is at 0.69. Modern portfolio theory suggests that when combining imperfectly correlated assets, total volatility is reduced.

Performance

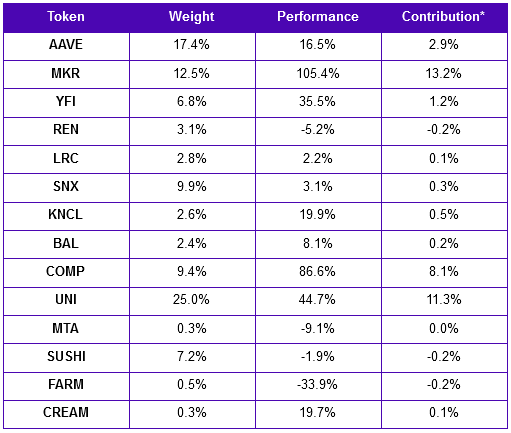

Turning to performance, April was a big month for the “boomer” DeFi large cap names MKR and COMP. MKR soared +105.4% while COMP was up +86.6%. The largest detractor to DPI’s performance was FARM, down -33.9%.

Top Performance Contributors

MKR: MKR was the top contributor in April after members of the MakerDAO community approved an executive vote to allow an ERC20 token representing ownership in a pool of real-world assets as collateral for DAI stablecoin loans. The loan was granted to New Silver, a real estate lending company. This was considered by many to be a step toward bringing potentially trillions of dollars of tangible assets such as residential real estate to the rapidly growing DeFi industry.

The governance token jumped +55% in the week the proposal was approved to top $4,000 per token for the first time in its trading history.

COMP: COMP was the second largest contributor to performance in the month following a relatively flat March. Total value locked in the Compound protocol surpassed $10B making it the first DeFi protocol to accomplish the feat.

Building on their success, the Compound community allocated 5,000 COMP tokens for a grants program in March. In April, the second round of funding took place bringing the total number of grants up to 13. The grants program was initiated in order to incentivize community members to propose protocol updates and new products that build on the Compound base layer. Ecosystem growth is important to the long-term success of a protocol and the market may be reacting favorably to what is becoming a robust grants program pipeline.

Top Performance Detractors

FARM: Harvest Finance’s FARM token struggled during the month of April after it was announced Sushiswap’s 2/3rds vesting program would go directly to individuals that staked rather than the protocols themselves. FARM had previously rallied on news of a proposal to the Sushiswap community to hold the vested SUSHI with a 1 year lockup and 2 year vesting. If Harvest Finance would have received the vested SUSHI, it was estimated to have an enormous impact on book value. Unfortunately, this was not the case and the token reflected the news.

Since FARM only represents about 0.5% of the total DPI index, the impact of the month’s negative performance was minimal, only resulting in a bottom-line decline of -0.2%.

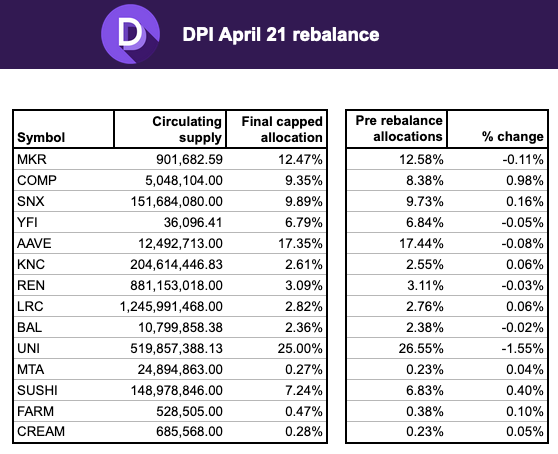

Rebalancing Summary

The DPI rebalance this month was relatively stable. MKR, YFI, AAVE, REN, BAL and UNI were trimmed in favor of COMP, SNX, KNC, LRC, MTA, SUSHI, FARM and CREAM.

Of note, the decrease in UNI allocation is partially due to an asset weighting cap of 25% as outlined under methodology v0.3. This is in accordance with the vision of DPI providing diversified and broad exposure across the DeFi market.

No new token additions were included in April.

Be sure to subscribe below for future updates on DPI.